Posts

The Bright-Line Changes

It is no secret that New Zealand is in the midst of a housing crisis. The housing crisis has been well documented in the media and has been a key political issue as successive Governments have searched for ways to create affordable rental housing and make homeownership an achievable proposition for New Zealanders.

However, as house prices have continued to increase considerably faster than incomes, the dream of homeownership has continued to be out of reach for many New Zealanders.

On 23 March 2021, the Government announced a range of measures intended to address the issues currently impacting the supply and demand for residential properties.

One of those measures included an extension of the bright-line test to 10 years.

Current bright-line test

The current bright-line test means if you sell a residential property (acquired on or after 29 March 2018) within 5 years after acquiring it you will be required to pay income tax on any profit made through the property increasing in value. There are some current exceptions including exceptions for the owner’s main home and for inherited properties.

Proposed changes to the bright-line test

The Government has announced that it intends to extend the bright-line period from 5 years to 10 years for residential property acquired on or after 27 March 2021. There will be exceptions for:

- Those properties that have been the owner’s main home for the entire time they owned it. These properties will be exempt from all bright-line tests.

- Inherited properties, which will remain exempt from all bright-line tests.

- New builds, which will retain the current 5-year bright-line period.

What do these proposed changes to the bright-line test mean for you if you acquire a property on or after 27 March 2021?

- If you sell the property more than 10 years after acquiring it (or more than 5 years for a new build), you will not pay tax under the bright-line test on any gain in value.

- If you sell the property within 10 years of acquiring it (or within 5 years for a new build), and the property was your main home for the entire time you owned it, you will not pay tax under the bright-line test on any gain in value. However, if the property was your main home, but was used for other purposes for more than 12 months during the time you owned it, you must pay income tax on a proportion of the profit from the gain in value.

- If you sell the property within 10 years of acquiring it (or 5 years for a new build), and it was never your main home for the entire time you owned it, you will pay tax under the bright-line test on any gain in value.

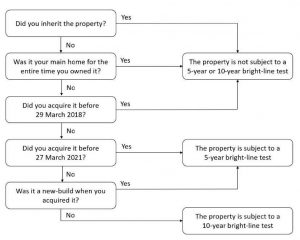

The IRD have issued the following flowchart which assists in identifying whether the bright-line test will apply, and if applicable, which bright-line period will apply:

Source: IRD

Please contact us should you require further information about the proposed changes to the bright-line test including:

- Clarifying when a property is deemed to have been ‘acquired’ for the purposes of these changes.

- Understanding what constitutes a ‘new build’ in order to qualify for the 5 year bright-line period.

- Interpreting the ‘change of use’ rule, which affects the way that the bright-line tax is calculated if the property was not used as your main home for more than 12 months during the applicable bright-line period.

In addition to the changes to the bright-line test, the Government also announced the following proposed measures:

- The intention to remove interest deductions on residential properties (except for new builds) – this measure is subject to further consultation and intended to be applicable from 1 October 2021.

- An increase in the income and price caps for First Home Grants and Loans

- The establishment of a $3.8 billion fund to accelerate housing supply in the short term.

- The provision of support for Kainga Ora to borrow an additional $2 billion to commence a land acquisition programme and increase housing supply.

We will provide further information on the above measures as and when they become available. In the meantime, please do not hesitate to contact us with any queries.

Please note that:

- there are other rules in the Income Tax Act 2007 that can tax gains on the sale of land, including residential land. Regardless of the bright-line test, anytime you purchase property with the intention of selling it you will be liable to pay tax on the profit unless an exemption applies.

- this article does not constitute legal advice, if you wish to understand the potential implications of the changes for your particular circumstances please get in contact with your advisor.